What is a compulsory portion in Austria?

What is a compulsory portion in Austria?

In Austria, every person is free to decide whom to appoint as heir in his or her will. This freedom is limited by the compulsory portion. The compulsory portion is a part of the assets that cannot be freely disposed of.

The right to a compulsory portion thus limits the freedom to dispose of one’s own assets upon death.

It therefore limits the freedom to make a will.

Only the following persons have a right to a compulsory portion:

Only the following persons have a right to a compulsory portion:

- Spouse or registered partner and

- descendants of the deceased, i.e. children, grandchildren, great-grandchildren, etc….

These persons are abstractly entitled to a compulsory portion.

On the other hand, siblings, nephews or nieces, unmarried partners or parents never have a right to a compulsory portion.

Therefore, if a person is not married (“registered partnerships” included) and does not have any children, he or she does not need to be concerned about the right to a compulsory portion. Such a person can freely dispose of all his or her assets. They could, for example, bequeath it in its entirety to the animal welfare association.

However, only being entitled to a compulsory portion in the abstract is not sufficient to have a right to a compulsory portion. This is because spouses and descendants are only entitled to a compulsory portion in concrete terms if they would also have inherited something according to the intestate succession. Thus, it must be examined which of the abstract beneficiaries of the compulsory portion would have come into play if the deceased had not made a will.

However, only being entitled to a compulsory portion in the abstract is not sufficient to have a right to a compulsory portion. This is because spouses and descendants are only entitled to a compulsory portion in concrete terms if they would also have inherited something according to the intestate succession. Thus, it must be examined which of the abstract beneficiaries of the compulsory portion would have come into play if the deceased had not made a will.

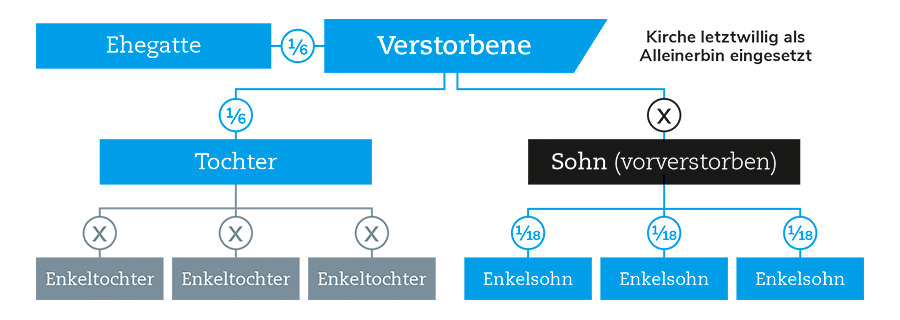

The deceased grandmother appointed the Church as her sole heir in her will. She leaves behind a spouse and a living daughter. This daughter in turn has three daughters (three granddaughters). The deceased also had a son. The son died earlier, but he in turn left three sons.

The deceased grandmother appointed the Church as her sole heir in her will. She leaves behind a spouse and a living daughter. This daughter in turn has three daughters (three granddaughters). The deceased also had a son. The son died earlier, but he in turn left three sons.

The spouse, the daughter and the three grandsons are entitled to a compulsory portion in concrete terms, but not the granddaughters. This is because the granddaughters would not be entitled to inherit even according to the intestate succession.

The spouse’s and daughter’s legal share of inheritance is 1/3, half of which is the compulsory share, i.e. 1/6 each.

The compulsory share of the grandsons is 1/18 each, because their legal share of the inheritance is 1/9 each: they share the third allotted to their predeceased father.

The deceased had appointed her unmarried partner as her sole heir. Her assets are limited to the last jointly occupied flat, a large condominium of considerable value in a prime location. The partner receives a pension of a medium amount and has no significant assets of his own. The deceased did not include her three children in her will.

In her will, the deceased also stipulated that her partner would not have to pay the compulsory portion until five years after her death. This is because her partner should not be forced to sell or encumber the flat in order to pay the children’s compulsory portion claims.

The partner can nevertheless settle the compulsory portion claims earlier if he wishes to do so. This saves him the interest of 4% per year.

{kind=link}

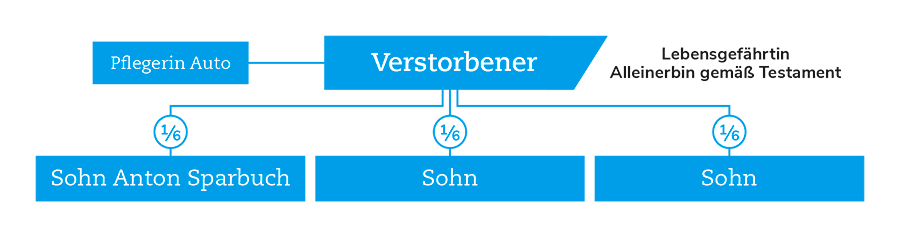

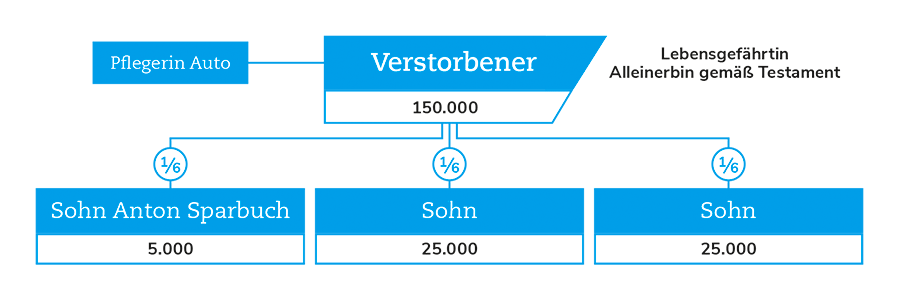

The deceased gave his car worth € 30,000 to his carer shortly before his death. He also gave his son Anton a savings book worth € 20,000 twenty years ago. The pure estate amounts to € 100,000. In addition to Anton, the deceased left two other sons, and he appointed his unmarried partner as his sole heir.

The deceased gave his car worth € 30,000 to his carer shortly before his death. He also gave his son Anton a savings book worth € 20,000 twenty years ago. The pure estate amounts to € 100,000. In addition to Anton, the deceased left two other sons, and he appointed his unmarried partner as his sole heir.

The assessment basis for the assessment of the compulsory portions after the addition of the gifts subject to imputation amounts to € 150,000 (= € 100,000 pure estate + € 30,000 value of the car + € 20,000 value of the savings book). The compulsory portion of the sons is 1/6 each, which results in € 25,000.00 each. However, Anton has to take into account the gift of the savings book worth € 20,000, so he only receives € 5,000. His brothers, on the other hand, each receive the full € 25,000.

Without addition and crediting, all sons would have received € 16,666.67 (= 1/6 of the pure estate of € 100,000). The addition and crediting of the gift to the carer and the resulting increase in the compulsory portions of the two other sons are at the expense of the sole heir, i.e. they reduce the inheritance of the partner. In the end, she only receives € 45,000 (= € 100,000 – € 5,000 – € 25,000 – € 25,000) instead of € 50,000 (without imputation).

Of course, an illegitimate child also has a right to a compulsory portion in Austria.

Whether a child is legitimate or illegitimate is irrelevant in Austrian inheritance law.